At American Insurance Brokers, we are highly experienced in everything related to truck insurance. You can always reach out to us if you have questions about how commercial trucking insurance works, which types of coverage are best for your needs, or other questions related to the industry. We have also compiled some of our most frequently asked questions below, along with simple answers that can help you get started.

- American Insurance Brokers, Inc.

69142 Highway 59, Suite A

Mandeville, LA 70471-7771

Toll Free: (800) 256-1177

Fax: (985) 871-1779

info@aibtrucker.com

Frequently Asked Questions About Commercial Trucking Insurance

What Does Commercial Truck Insurance Cover?

State-specific commercial truck insurance regulations mean that depending on where you are, different coverages may be available. We offer the following types of commercial truck insurance.

Commercial Auto Liability

When you are at fault for an accident, commercial auto liability insurance pays for any property damage or injuries to third parties. In the event of a lawsuit, it might also cover the expense of your defense.

Physical Damage

The word “physical damage” refers to a variety of insurance policies that can safeguard your truck. This often includes comprehensive insurance, fire, and theft with combined additional coverage (CAC), and collision insurance.

Medical Payments Coverage

This can cover medical costs for you and any passengers in your car who get wounded in an accident. It is also known as MedPay coverage. The coverage generally covers the insured and their passengers regardless of who caused the accident.

Uninsured Motorist Coverage

Depending on the state, this category of insurance may include three distinct insurance products that are frequently lumped together. If you get into an accident with someone who is either uninsured or underinsured, this coverage can protect you.

Trailer Interchange Insurance

Trailers being pulled in accordance with a trailer exchange agreement require this kind of physical damage insurance. If the trailer is destroyed by a collision, fire, theft, explosion, or vandalism, this insurance could offer you financial security.

On-Hook Towing Protection

If a vehicle you do not own is damaged due to a collision, fire, theft, explosion, or vandalism while you are towing or hauling, on-hook towing insurance may cover the cost of repair or replacement. Note that garage keepers’ legal liability insurance is the name given to on-hook towing insurance in Texas.

Legal Liability Insurance for Garage Owners

Business owners who own service stations or provide towing services might be protected by garage keepers’ legal liability insurance. When you keep a customer’s vehicle in a covered area for parking, storage, or service, it must be protected. Keep in mind that Texas refers to storage facility insurance as garage keepers’ legal liability coverage.

Workers’ Compensation Insurance

Workers’ compensation insurance, usually referred to as workers’ comp, is a type of insurance that all kinds of enterprises and sectors are required to carry. When an employee gets hurt at work, it typically pays for their medical bills as well as a portion of their lost salary. Additionally, it can shield businesses from claims based on working conditions.

How Much Does Commercial Trucking Insurance Cost?

There is no straightforward answer to this question that applies to all situations because there are many factors that go into the cost of commercial trucking insurance. They include:

There is no straightforward answer to this question that applies to all situations because there are many factors that go into the cost of commercial trucking insurance. They include:

- Cargo: The type of cargo that a truck is hauling is a crucial consideration. This is because some things are riskier to carry. For instance, it will undoubtedly cost more to insure a car carrier with a dozen vehicles than a truck hauling produce. The car carrier will probably do more damage in an accident. Transporting hazardous items is another significant factor that could raise the cost of your insurance.

- The type of insured vehicle: The type of insurance required by trucking businesses will vary. Large semi-trucks are more capable of causing damage than tow trucks, hence their insurance costs are typically higher. Additionally, newer vehicles often cost more to insure because they are more expensive to fix or replace after an accident.

- Route: Trucks working in a wider area are typically more at risk. Longer journeys could include busier times and possibly unfamiliar highways. A truck with a regular, short route will normally pay less for various truck insurance policies.

- Location: State-specific insurance premiums also differ. Due to increased traffic, adverse weather, and other considerations, some geographic regions will simply cost more.

- Driving History: Like a personal auto insurance policy, driving history is a significant cost-determining element. Because of how serious a collision with a huge vehicle is likely to be, accidents and moving offenses will increase your premium. Depending on the size of your fleet, maintaining a spotless driving record could result in monthly savings of hundreds of dollars or more.

At American Insurance Brokers, we put in a lot of effort to find our clients the best deals. We can put together a plan with various truck insurance options that offer security while being within your price range.

Frequently Asked Questions About Motor Truck Cargo Insurance

What Does Motor Truck Cargo Insurance Cover?

Cargo you haul for a shipper is covered by motor truck cargo insurance. You determine the limit when you choose your policy.

Am I Required by Federal Law To Carry Motor Truck Cargo?

No, but it is common for shipping companies to require it.

How Much Motor Cargo Insurance Do I Need?

Ask the company you are hauling for what their cargo coverage requirements are.

Bobtail / Non-Trucking Liability / Deadhead Insurance

What is the Difference Between Non-Trucking Liability, Bobtail, and Deadhead Coverage?

These are all different terms for the same type of coverage. They provide coverage protection for your truck when you are off the job. For example, they would cover you when you are getting your truck repaired or getting it washed.

What Do I Need in Order to Obtain Bobtail/Non-Trucking Liability Coverage?

- A lease agreement that is longer than 30 days

- Truck year, make, and VIN

- Driver’s name, license number, and date of birth

- Loss payee information (for physical damage only)

- 3 Years of experience (in most cases)

Why do I need Bobtail/Non-Trucking Liability Insurance?

The company you haul for only covers your insurance while you are under dispatch for them. When you are not under dispatch, for example, if you are having your truck washed or getting an oil change, the bobtail/non-trucking liability policy protects you.

What happens if I change the company I am leased to?

When changing a lease agreement, fax a copy of the new lease to our office at 985-871-1779. Also, fax a request for us to change your policy to reflect the new company you are working for.

Frequently Asked Questions About ICC Authority / MC Authority Insurance

What is ICC Authority/MC Authority?

Before you can legally operate as an interstate regulated carrier, you must be granted permission from the Federal Highway Admission in Washington DC. Your ICC authority is permission granted by the federal government to transport regulated freight across state lines (Interstate).

Who is Required to Have ICC Authority / MC Authority?

Any vehicle operating for hire in interstate transportation of regulated freight or passengers must have operating authority.

Who is Exempt from the Requirement for ICC Authority / MC Authority?

Private carriers that transport their own cargo, “for-hire” carriers that exclusively haul cargo that is not federally regulated and carriers that operate exclusively within a federally designated “commercial zone” that is exempt from interstate authority rules are exempt from requirements for ICC Authority / MC Authority.

What is the Minimum Insurance Coverage Required to Obtain an MC Number / ICC Authority?

If your vehicle has a gross vehicle weight rating (GVWR) of 10,000 pounds or more, the following is required:

- $750,000 (BI &PD) for general commodities (non-hazardous)

- $1 Million (BI &PD) for hazardous materials except for class A & B explosives

- $5 Million (BI & PD) Class A & B explosives, hazardous materials transported in specified capacities in tanks or hoppers, and/or any quantity of hazardous materials as specified in 49 CFR 173.403 of the Federal Motor Carrier Regulations.

If your vehicle has a GVWR of less than 10,000 pounds, the following is required:

- $300,000 (BI & PD) for general commodities except any materials listed

below - $5 Million (BI & PD) Any quantity of Class A or B explosives, for any quantity

of Poison Gas (Poison A) or highway route-controlled quantity of radioactive

materials

Brokers must maintain a surety bond or trust fund in the amount of $10,000. We can arrange this for you.

Frequently Asked Questions About CSA

What is CSA?

CSA is an FMCSA safety program to improve large truck and bus safety and ultimately reduce crashes, injuries, and fatalities related to commercial motor vehicles. Its enforcement and compliance model allows FMCSA and its state partners to contact more carriers earlier to address safety deficiencies before crashes occur. The program established a new nationwide system for making the roads safer for motor carriers and the public alike.

When originally rolled out, CSA stood for “Comprehensive Safety Analysis 2010.” However, as the national implementation of CSA rolled out in December 2010, the Federal Motor Carrier Safety Administration (FMCSA) transitioned the program, removing the “2010” and renaming the initiative “Compliance, Safety, Accountability.”

What Regulation Forms Do Carriers and Drivers Need to Fill Out for CSA?

No one needs to register for CSA, nor is there any kind of mandatory training requirement. However, it is in commercial motor vehicle carriers’ and drivers’ best interests to be informed about CSA and what it means for them. The Federal Motor Carrier Safety Administration’s CSA program impacts all carriers that:

-

- Are over 10,000 pounds

- Travel on the interstate

CSA also impacts carriers that haul hazardous materials intrastate.

How Can Commercial Motor Vehicle (CMV) Carriers Successfully Navigate CSA?

Check, update, and review your records. Start by ensuring that your motor carrier census form (MCS-150) is up-to-date and accurate.

Monitor and review your Behavior Analysis and Safety Improvement Category (BASIC)

percentile ranks as well as inspection and crash data in the Safety Measurement System (SMS) and the Federal Motor Carrier Safety Administration (FMCSA) Portal.

Maintain copies of inspection reports and evidence related to any observed violations and request review of any potentially incorrect data using DataQs.

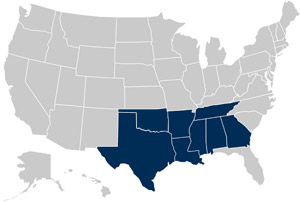

Truck insurance coverage in Texas, Louisiana,

Arkansas, Mississippi, Alabama, Georgia & Tennessee.

Free Coverage Review

Receive a free review of your current

commercial truck insurance policy, including

multiple competitive quotes & an independent consultation from our experts in Mandeville, Louisiana.

» get your free coverage review now!

![]()